Why Create a Dept. of Gov Efficiency: an Econ Crash Course

How bad is America’s debt situation? Where is it headed? What solutions are left?

Subscriber Note

Hi! I’m taking a bit of a detour from the planned posts here. Sorry. Like many, my eyes for the last month have been on the US election. While there hasn’t exactly been a shortage of overall coverage there (ha), my forever interest is in taking a closer look at important individual stories that I don’t think have been covered well.

I ended up landing on two this time, both of which I’m approaching from a nonpartisan POV. I’m not a US voter, and I don’t think many readers are dying for more team-based coverage anyway.

The point in this first one isn’t to take a fixed stance on the DOGE project in terms of its likely outcome, which feels unknowable to me. It’s to look at the big picture of the why behind it. Because say that Kamala had won. Would it be a good or bad idea for her team to consider a similar effort in rethinking government spending? How urgent is the need? And what would useful cuts or changes even look like?

There’s been public handwringing about rising national debts for decades. But there hasn’t been much in the way of explanations in plain language, where an average reader can sit down for 20ish minutes and walk away with a clear and measured sense of the problem from end to end. So it’s my goal to supply exactly that here. While it’s true that the economic sky hasn’t fallen yet, should we expect that to remain true? And what realistically can be done? I consider these important questions.

If you’re not in for a long read, you can find a summary version here.

Introduction

President Trump announced this week that entrepreneurs Elon Musk and Vivek Ramaswamy will lead his new Department of Government Efficiency (DOGE).1 Their mandate will be to “slash excess regulations, cut wasteful expenditures, and restructure federal agencies”, with a deadline of July 4th, 2026.

To understand why a project like this might be both necessary and urgent, we have to look at what’s been happening with inflation. Not just what happened during the COVID years, but the structural stuff that’s been coming to a boil for decades—and how it relates to government spending and debt.

My goal here is to provide a politically-neutral 101 explainer on four big questions:

Just how dark is America’s current financial pathway? (Very. Every government budget agency says it’s unsustainable.)

What realistically can be done about it? (Roughly eight things, though four are unworkable.)

Of those possible solutions, is something like DOGE necessary? (It’s likely riskier to not try.)

What would useful cuts and changes look like? (Long answer.)

All the data I’ll be using here comes from nonpartisan government sources, which all tell the same troubling story. To quote just the first sentence of a recent assessment from the Government Accountability Office: “The federal government faces an unsustainable fiscal future.” The rest of the report is not rosier.

DOGE is one attempt to back America away from a cliff. Whatever you’ve heard about it, and whatever your personal politics are, I reckon it’s helpful to ground our debates on a clear view of the underlying economic dynamics. Because they’re grim, and delaying urgent action will only make future pain all the greater.

I’m going to simplify things here a lot to make it easier for general readers. If anyone feels that anything is wrong or misleading, let me know using this anonymous Typeform or via a comment in this discussion doc. I’ll address all concerns and FAQ there so that readers don’t have to track conversations across the whole internet.

While my work life has been American-centric for years, I’m not a US citizen. Even so I’m going to use “we” and “our” here just for simplicity’s sake.

Even if you aren’t American either, most of what’s true here is true for other countries too. And what happens to the American economy will ripple to every global shore.

The Foundation

Before we can really talk about government spending, we have to start with the foundation—with the thing that allows us to have money and wealth and debt in the first place: productive labor.

Everything that we make or do that someone else will pay for has economic value. Whenever you swing a hammer or hammer away at your keyboard, if you’re being paid for it then you’re creating economic value that didn’t exist before. We then measure this collective value creation as Gross Domestic Product (GDP). Basically anything that has a legal price tag counts towards it.2 The dollar value of every home built, every ticket sold, and every Big Mac served is added together, and that grand total is our country’s GDP—our national scoreboard for how much useful work we got done.

If we’re trying to understand whether we’re working harder and smarter over time, we also need that scoreboard to account for inflation. If I raised my rates by $20/hr this year simply because I saw other prices going up, then our GDP needs to be discounted accordingly. Because I didn’t provide extra value per hour for that extra money; I just charged more. Economists call this adjusted figure real GDP, which can also be calculated on a per capita (person) and per hour basis to give us even more insight.

Using these lenses helps us interpret the big scoreboard more clearly. If GDP goes up in a given year, we want to understand how much of this was just due to adding more workers to the economy, how much was simply a rise in prices, and how much was us actually producing more value per hour of work. Because the last one is what really tells us how much richer we’re getting. Just adding more workers to grow total GDP can have diminishing benefits3, while increasing average productivity is the great long-term wealth engine. If your machine shop figures out how to make more widgets for the same amount of wages, you’re helping the nation’s real GDP per capita tick up. If every other company does the same, the good times will roll.

A healthy economy wants to grow this number by a few percent a year, especially when they're also taking on a lot of new debt. While most countries can manage the odd low year (say a pandemic), falling too far behind for too long is how you get to the bad place. And you really don’t want to end up in the bad place.

The Role of Government Debt

There’s a GDP cheat code of sorts, which can be used well or poorly. Any government that’s already rich enough can simply invent extra money by creating and selling new loans (ie. debt), and then spend that money on things like bridges, power plants, and science labs—with the hope that these investments will help unlock enough additional future GDP to pay back the loans and then some.

To get this money back, the federal government typically collects about 17% of annual GDP in taxes, with the understanding that it will use this income to both pay down debt and invest in other new projects that it expects will foster even more future productivity. When these loans work and real GDP per capita goes up as a result, the government makes more money even if it keeps tax rates the same, as it’s now getting the same share of a larger pie. Done right, this is the virtuous cycle that makes countries rich and keeps them that way.

Good vs. Bad Debt

How much GDP growth a country needs depends a lot on its debt. While more growth is generally better, it mostly needs to grow GDP fast enough to stay ahead of its debt repayments. Otherwise it will eventually need to permanently raise taxes, double down with new debt, or do something even less sustainable.

This in mind, countries want to spend heavily on the things most likely to increase future GDP. Good examples include giving out grants to promising students, retraining workers to more productive fields, and improving infrastructure that all businesses can use—like highways and the internet.

This isn’t to say that every dollar that the government spends needs to have a direct and/or guaranteed effect on GDP over some set time period. There are investments that either pay back very slowly or that have indirect benefits that most of us still think are important.

Basic science research is a lot of fumbling around in the dark, where outcomes are unknowable. But if we’re funding sufficiently talented researchers, their discoveries can sometimes unleash enormous long-term productive gains.

Free school lunches may take a decade or more to pay back for themselves. But if we believe that students who are less hungry during school are likely to learn more and eventually find better jobs than they would have otherwise, this can be an excellent investment.

It’s also good to maintain a country where people are just generally happy, healthy, and safe—and where the world’s best workers want to live. So it makes sense to also invest in having eg. attractive national parks, a dependable legal system, and a few more firefighters than you think you need.

While measuring these things is always a bit imprecise, countries that fund a healthy amount of them often end up with higher GDPs than countries that don’t. In general it's easier to be productive when you have fewer things to worry about and more nice things to enjoy in your down time.

Of course though, these programs can have the right idea but still be inefficient. We need government executives to be vigilant about pushing for the right balance of value and cost—not to the point of stinginess, but with the goal of ensuring the public is getting a reasonable and sustainable return on their money.

Where Inflation Comes From

There’s a way in which inflation is obvious to everyone, and a way in which PhDs study it for decades and still have intense fights about it.

One simplified view is that inflation happens when the amount of money sloshing around outpaces the creation of things you can buy with it. Given that a country—or the world—only produces so many goods and services, an over-increase in the money supply will lead to more demand (total dollars we’re willing to spend) than supply (the total stuff we can buy). The natural result is that prices go up. While a bit of this is ok (say 2% per year4), too much of it leads to what we’ve seen since COVID.

How does this happen? What causes the money supply to suddenly outpace economic growth itself? Well, a few things. A big one is low unemployment, where there aren’t enough workers available so companies need to pay more to get their share. Another is what we saw during COVID, where freak events disrupt our ability to make and do stuff. If a lot of factory workers are sent to shelter at home, there will be fewer cars and toilet paper rolls made for us to buy. If our incomes also go up a bit thanks to emergency government benefits, we’ll be bidding against each other at higher and higher prices to get the stuff we want. And as prices go up we’ll all naturally want our wages to go up too, which will push prices up even further etc.

While these were big factors in the inflation we’ve seen since 2020, they aren’t the whole story though. There are four other crucial forces we need to consider:

The impact of all the money the government borrowed during the pandemic

The growing federal deficit (ie. how much more money it needs to borrow each year)

The mismatch between people retiring from the workforce and the number of new births

The effect of a thing called Baumol’s cost disease

The unfortunate net result here is that inflation will be a metastasizing problem over the years to come—where all the options available to tame it will be more drastic than many assume. While we’re not at the cliff yet, we’ve gotten a lot closer, and we’re driving much faster towards it.

To get a clearer sense of all this, let’s look at each of those four dynamics in order.

Pandemic Debt

The financial impact of the COVID era was brutal. How bad? One way economists measure this is by dividing a country’s GDP by its national debt. This lets us compare how much new debt was taken on relative to the economic growth it unleashed. In a perfect world this ratio would go up when governments borrow for big projects like building interstate highways, before falling back down as those new highways are used by companies to ship goods faster to create more taxable GDP. While we want some big bets here, it’s generally good to chase a long-term balance.5

Anyway, while this isn’t the place for a political discussion about how the US government responded to the pandemic (there were hard tradeoffs involved), the outcome of it all was a much worse debt/GDP ratio.

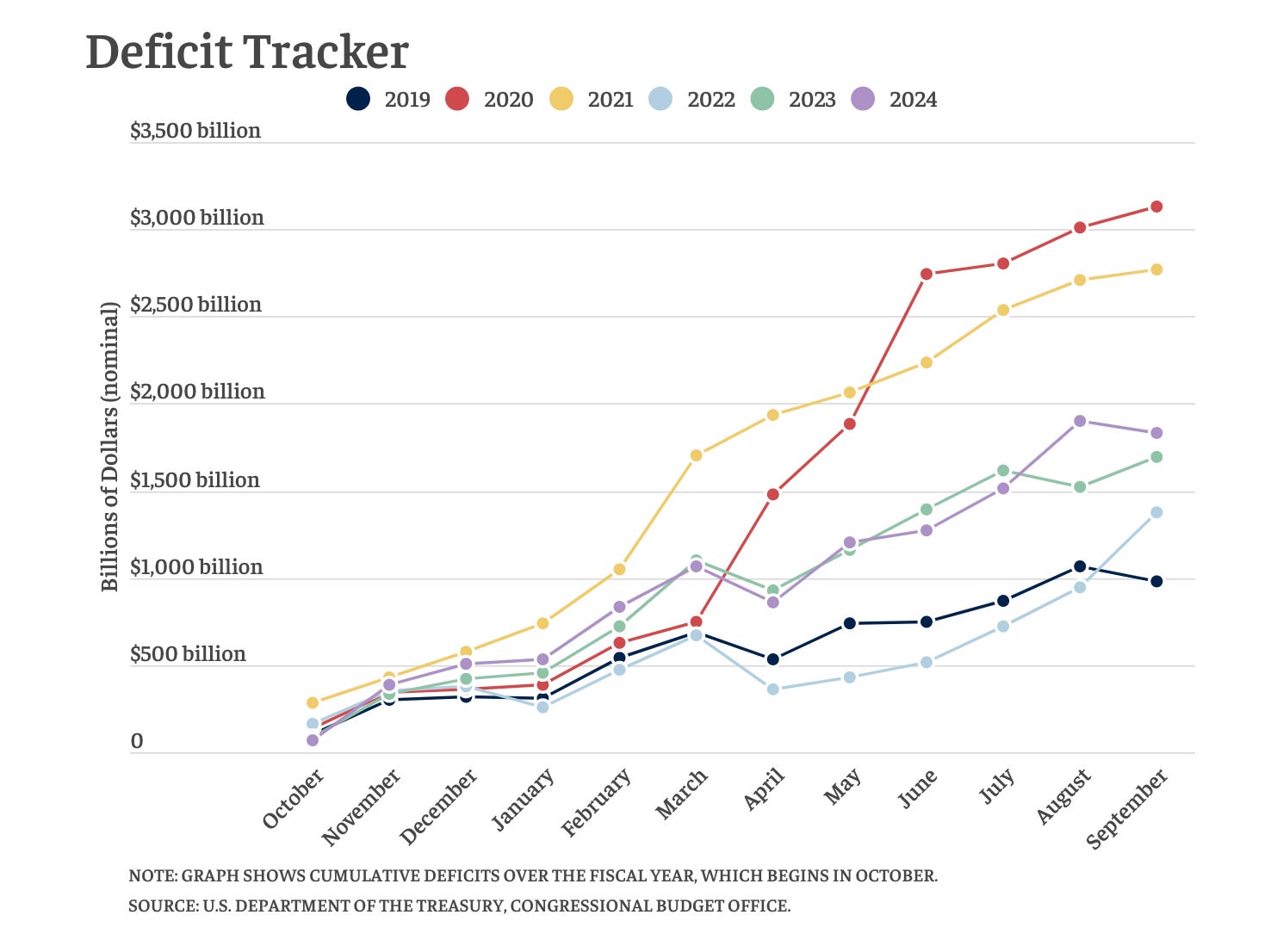

Here’s a chart for the last 10 years, with a very obvious spike in 2020:

The total dollar value of all US federal debt before the pandemic was just shy of 107% of the country’s GDP. It’s now about 120%. To put that in perspective, the US produced $27.4T in GDP last year, of which the federal government collected $4.4T in taxes. Its total debt is now just shy of $36T, or over eight years worth of all federal taxes combined. And this doesn’t include state or municipal debt that may one day become its problem. It’s…a lot.

Is this going to get better on its own? Oh, no. Very no. Extremely no. Quoting from the Treasury Department’s latest annual report:

If current policy is left unchanged, the projections show the debt-to-GDP ratio will be approximately 100 percent in 2024, rise to 200 percent by 2047 and reach 531 percent in 2098.

This obviously isn’t all, or even mostly, a COVID thing. But the pandemic’s aftermath left America with even less runway to make the deep structural changes that it’s long put off. And while the shock inflation of 2022 has died down, prices are still going up at about 3% a year, with no sign of easier days ahead.

The Federal Deficit

The mismatch between how much money the federal government raises in taxes (and tariffs etc) in a given year and how much it spends is the federal deficit. And every dollar in federal deficit generally means a new dollar of national debt.

While we saw much larger deficits over the pandemic years, America is still going deeper into the red at about $1.8T per year (see the light purple line):

The main problem with this is that payments on this debt are taking up a larger and larger share of the government’s total budget. Thanks to newly high interest rates, they’ll make up a higher share of spending in 2024 than Medicare or National Defense!

And this isn’t to pay off any debt. It’s just to make the interest payments. The actual debt itself is mostly just being rolled over, thus creating a new set of replacement interest payments for tomorrow. Rinse, repeat.

Now, how does this affect inflation? Unless the American economy begins growing much faster, the government will be forced to issue ever-increasing amounts of new debt to keep up with payments on the old. And when you create new money that’s not matched or followed with real economic growth, inflation makes up the gap. While this can be managed by raising taxes and/or interest rates, what’s that going to do to future GDP? Either the economy starts booming or it’s pick your poison.

Cue the next bit of bad news: real GDP growth per capita is about to get much harder to come by.

The Retirement Boom

When a worker begins receiving federal retirement benefits like social security and Medicare, they generally leave the workforce. Even if some of them continue to work a little here and there for extra income, their contributions to GDP are going to fall off hard. They’re no longer helping as much in making cars, delivering Amazon packages, and building new houses. This means real GDP per capita goes down.

In a country with say twice as many baby births as retirements each year, this isn’t a big deal. But the US is no longer such a country, nor even close. Baby Boomers got their name from a lot of them having been born around the same time, and over four million of them are now retiring each year. Meanwhile new births are pacing several hundred thousand behind that. This is a very big problem!

And while it’s quite lovely that retirees are living longer than ever6, longer lifespans mean more checks cashed and more healthcare used. And if we aren’t replacing retirees with enough new workers, that means fewer nurses and oncologists in the workforce at the moment we need them most. This mismatch between demand and supply? You guessed it, more inflation! And this has a recursive effect. When prices go up, social security checks have to go up too. And so on, forever.

And even after all that, we’re still not quite done yet.

Baumol’s Cost Disease

Machines and computers get more efficient over time in a way that humans alone can’t. A delivery app can grow to take 10,000 orders in the same time as it can take 100, whereas a human can (mostly) only take one at a time and can only work one hour in an hour. This creates a growing split in the market between companies that use a lot of machines and those that don’t. The first group gets far more efficient over time, producing more GDP per worker hour, while the second improves slowly, if at all.

More productive companies also generally make higher profits, which allows them to pay higher wages without having to change prices.7 But what do we do about wages at a company where productivity has peaked? Take, say, a community theater actor. They can’t just speak their lines twice as fast and charge twice as much. Yet their rent and food costs are going up. What do we do about them?

We could just go without their services in favor of more impersonal alternatives, as we once did for eg. milkmen, elevator operators, and Blockbuster employees.

We could simply pay them more, in the form of ever increasing prices. While we could get our lattes from a machine, it’s nicer to get them from a barista. And maybe we find this luxury worth it. Sure it may cause a bit of inflation, but a little bit is fine as a treat.

The problem is scale. Propping up less productive jobs leads to an effect called Baumol’s cost disease. And it isn’t always as wholesome as keeping used bookstores alive by overpaying for dog-eared copies of The Hobbit. Cost disease is why, for example, college tuition keeps skyrocketing. Universities employ a lot of people, and most of them are in unions that push hard for higher wages even when productivity is going down. As most students believe (rightly or wrongly) that they need degrees, they sigh and swallow the tuition increases. But eventually these costs grow so large that some degrees become more noose than boost.

The killer is that cost disease is irreversible. It chases people into more productive jobs, eating the ones they left behind. But what happens when workers can’t move up anymore? While new positions will open at the most productive companies, what if you don’t qualify for one? Eventually the government has to step in to cover the gap with some combination of tax cuts/credits, tuition forgiveness, basic incomes, and minimum wage guarantees.8 But what’s the net outcome of all those moves? When you’re boosting the money supply beyond what productivity can pay back, it’s inflation all the way down.

A Sidebar on Taxes

Some readers may think I’m skirting the obvious: can’t we just tax the rich more? If they work for productive companies (or own them), isn’t it reasonable to ask them for more of their winnings?

While there’s an attractive idea of economic justice here, this only helps in the long run when that redistribution is driving new productivity somewhere in the economy. If I take a million dollars from Elon Musk and use it to start a successful software company, that math works fine. The same would be true if I spent it all on goods and services from highly productive companies, as that would be economically the same as him spending it. The problem is that I’m much less likely than him to do both those things—which ends up mattering a lot. And the degree to which I do this worse is the degree to which I’m just accelerating both cost disease and inflation. Even if I give only say 20% of that money to low-productivity companies, this adds up!

In theory, the government should be extremely good at spending money in ways that unlock new productivity. And in theory we should be too. But we only have to get this math a little wrong for the system to fail over time. And with a national debt this high, the difference between a few points of GDP over say thirty years is the difference between flying cars and the lights going out across the Roman Empire.

Raising taxes is fine as a matter of fairness. But it only solves the underlying financial crisis to the degree that these taxes are spent well. And right now they aren’t. Not because I’m saying so, but because the government’s own charts say so! America’s debt-to-GDP ratio is on an unsustainable course, and has been for a while.

If we can get growth to where it needs to be, there will be many spoils to share. If we can’t, inflation will eat us alive. And while, yes, we can delay peak inflation by raising taxes and/or interest rates, the underlying problem will remain: either we find new growth or we choose how we wish to die.

A Final Dagger: Known Unknowns

Ok, now the real bad news: the numbers we’ve just gone through barely factor future spending on climate events, wars, pandemics, financial crises, or any other economic shocks. Nor do they include the money that the federal government is going to have to pay to bail out the states as their own similar budget issues come home to roost. As bad as the above numbers are, they reflect best-case scenarios where we dodge the catastrophes that have always happened and always will. Reality will be worse.

So, now: what can we do about all this?

The Seven Pathways

We’re at a weird time in human history. Productivity has basically stalled across the developed world, which governments have mostly papered over by simply borrowing more. Most of these countries are also seeing the same troubling trend with low birth rates, which just compounds the problem. It’s all a bit bleak.

That said, there are roughly seven theoretical solutions:

Write off some of the debt that the government owes itself

Reduce retirement benefits to grandma and grandpa

Raise the retirement age

Massively scale up skilled immigration

Massively scale up technological progress

Get more business owners to adapt existing technology

Massively shift government spending towards GDP enhancement

Of course, the first three of these aren’t really on the table:

In theory, the government could write off the share of its national debt that it owes to itself, 9 allowing it to shift more spending from interest payments to boosting the GDP. But this is a nuclear option, likely wouldn’t work, and the first rich country to try this is going to have a very bad time.

Cutting social security and/or Medicare benefits will make people very upset, and is generally political suicide to even talk about.

While there’s some fairness to raising the retirement age (as most benefit programs were designed with much shorter post-retirement lifespans in mind), the time to do this was twenty years ago. Boomers vote, and they’re likely to break in huge numbers away from anyone who tries this.

So that leaves us with the other four:

While skilled immigration is a huge positive, there are scaling limits. Some are social, some are logistical, and some just boil down to “those countries need skilled workers too, and it’s in America’s national and moral interests for those countries to grow their own economies a lot”. Even so, the US should certainly do a lot of this, and should especially target entrepreneurs.

The progress of breakthrough technologies—eg. AI, energy, biotech, rockets, robotics—could very well bail us out by unlocking historic productivity gains in a sort of economic Cambrian explosion. This is basically what the US and every other country is banking on. (We should be cheering this on! Booing and over-regulating the innovations that might save us is self-defeating!)

In theory, getting the 30-something million existing businesses in the US to upgrade their technology to the best of what’s already out there would help productivity a lot. But this has been the white whale of consultants for generations. I’ve been one, and have been dashed against the rocks of hope like all the rest.10 While it’s not impossible, it’s much, much, harder than you’d think. (The same dynamic applies to pushing workers into more technical jobs. It’s a great idea, and we already try hard to do it. But it’s easier imagined than done.)

To avoid putting all your eggs in the above three buckets, you could just create something exactly like the Department of Government Efficiency.

Of note, Musk happens to run giant companies working on five of the most promising breakthrough technologies. This isn’t a coincidence, and should cause more reflection than it probably will. If even he is looking at the math here and worrying about it, it’s at least possible that we should be more worried too. Though abundance is coming, that speed at which it materializes matters an awful lot.

Anyway, DOGE time.

The Outsiders

The Government Accountability Office was formed in 1921 to audit spending across the federal government and report back to both Congress and the general public. There’s also an Office of Management and Budget, the Council of the Inspectors General on Integrity and Efficiency, and a half-dozen more agencies with similar roles and titles. If they already exist, what’s the point of DOGE exactly?

One way of looking at it is that these groups, despite being quite clear on the urgency of the situation, have failed to get the government (and voters) to actually act urgently. Quoting from the most recent GAO report:

The federal government faces an unsustainable fiscal future. … The debt is growing because the country keeps borrowing to finance an increasingly large gap between government spending and revenue. … The underlying conditions of the problem have existed for over two decades.

Reading this, it isn’t insane to me to think that new and louder voices may be worth a try if we really want to shake up The Way Things Are Done. It’s often helpful to have outsiders to change a culture—and to take the heat.

Organizational DNA

Private businesses have to scrap to survive. Making hard decisions mostly isn’t optional. Layoffs, freezes, and firings are all part of normal operations, where not doing them can be a death sentence. While most federal agencies are hardly cozyspaces where productivity doesn’t matter, they are on average far more insulated from performance pressures. Managers also tend to be more reluctant to reduce headcount at the cost of losing budget share in future years, and their ultimate bosses are forever rotating in and out with elections and cabinet shuffles. The end result is a culture that often prizes outcomes more than efficiency.

Case in point, the GAO recently reported that US federal agencies made $175.1B in overpayments last year alone. That’s about 4% of total federal tax revenues. Or about the entire GDP of pre-war Ukraine, a middle-income country of over 30 million people. Or about 7x the cost of the entire US Pell Grant program, which pays for millions of poor kids to go to college every year. Adjusting for today’s dollar values, that money could have funded five Manhattan Projects. But it did not.

A good chunk of these overpayments were for pandemic-era benefits programs, where the logic looked very different in 2020. As the need then was getting money out as fast as possible to keep rents paid and GDP from cratering, a bit of slippage was a plausibly acceptable cost of getting that done. But these were payments made in 2023. While the optimal overpayment rate is never 0%, it’s not unreasonable to have wished that this number had been ruthlessly driven down much, much faster than it was.

It’s not that these agencies are full of clueless people. It’s that it’s not their money. They have meetings, set reduction goals, do some studies, and in the margins make a few good adjustments. But who is there to slam fists on tables and call for all-nighters and generally attack the root problems one by one until they’re fixed? Where’s that culture? And are we ever going to get it from culture-preserving incremental adjustments? What in reading past GAO reports would give you that confidence?

While some might argue that massively reducing overpayments could only be done with more headcount and spending—which is the opposite of what DOGE is proposing—this seems unimaginative to me. Picture a world in which the Biden administration had put out a call for teams of hungry young technical people to map out and attack these problems. The government could have played venture capitalist, getting some equity in return for their cash investments. Fund a few of them and not only do you increase your chances of eliminating waste, but in doing so you accelerate the next Plaid, Stripe, or Palantir and boost tomorrow’s real GDP a healthy amount—which is a very good trade for the American public.

Possible Criteria

Even if we accept the necessity of at least some urgent reform, what makes for a good cut or change vs a bad one?

The government spends a lot of money on a lot of things—from benefit payments to salaries to grants to reimbursements to a dozen other categories. The point shouldn’t be to reduce or eliminate this spending arbitrarily, nor equally. Judging from Musk and Ramaswamy’s comments, I’d expect them to look for:

Work being done inefficiently, either where the technology being used is poorly engineered, or where the whole approach is just needlessly bloated.

Work that overlaps with other agencies, where the target is all the duplicate efforts, slow decisions, high coordination costs, and vague accountability.

Work that can be done just as well by the private sector, where there’s thought given to what the private sector doesn’t want to do, can’t do fairly, can’t do securely, or can’t do at scale.

Work that’s blocking the private sector, where agencies are slowing down companies out of proportion to the real risks involved.

That last one is likely to get special focus. An overzealous regulator can pause billions in economic activity to conduct eg. environmental studies on relatively minor risks. If we’re talking about potential ecosystem collapse or irreversible contamination, then yes, obviously, the work has to wait. But if the worst outcome is, say, minor local habitat damage, I suspect DOGE will consider long delays to be a moral luxury.

I’d also expect for DOGE to demand things like:

More plain language communication for the public. Say a 1-2 page info sheet for each program that explains the key financials, the government’s thesis for how this spending will boost GDP (else what other benefit the public is getting), and the name of the person who owns that spending.

Plans for simplifying decision structures. While collaboration is often useful, there are rapidly diminishing returns to excess mandatory coordination. What if each program had a czar whose job it was to post a report every year about their experiments on reducing decision inputs to their useful sweet spot? Not an outside inspector with an audit checklist, but someone inside with a machete.

Plans for simplifying regulations and reporting requirements. These are often hideously structured, with businesses having to hire expensive consultants to even understand what’s being asked of them. Different agencies also often ask for different versions of the same data, else have arcane rules for how this data is submitted. We need czars to do a full rebuild, looking at the whole system from the POV of the end users whose focus we’d prefer to be on growing the economy.

Plans for simplifying taxes. The current tax code, understood in its full sense, is millions of words of rules and regulations and test cases. While a complete rebuild would be a monstrous undertaking, there are certainly chunks of it that could be rethought to make it easier for people to know how much they owe--and to ensure we're really taxing the right things.

It’s not that most (or even any) agencies are doing useless work. It’s that bloat is bloat, organizations shape themselves to their requirements, and sometimes radical restructuring is the only way to break through decades of institutional muscle memory. While spending on positive things is good, not all that spending is necessarily good! There are better ways to do most things! If DOGE goes in and finds nothing to improve or cut, they shouldn’t cut for the sake of cuts. If that government spending is already boosting GDP in a highly efficient way, confirming that is mission accomplished. But they also may find a surprising amount of fat.

Of course, there will also be political considerations. A conservative will propose different cuts than a liberal. As such, I’m sure that left-leaners will find more to object to in some of the specific cuts proposed over the months to come. I may too. That said, I suspect we’ll make our cases best by helping those program managers explain the impact of their work as clearly and publicly as possible, rather than by arguing against the basic premise that overall cuts might be good or needful.

(Criticisms about how DOGE goes about its work are also essential. They’ve promised to work transparently, and to engage widely as they go. I hope they do, and that public engagement is as vigorous as it is informed.)

Final Thoughts

Will DOGE work? I think people who’ve bet against Musk have been right sometimes and wrong more often. Will it all go to plan? Probably not! This is a hard and new and unusual thing. Those rarely go smoothly on first attempt. Given how power-sharing works in government and how bureaucratic all change is, this could not work in a dozen different ways.11 Even so, I hope that it’s tried, that the public (including journalists) engages helpfully, and that at least some of it works.

What I do know is that failing to grow GDP is no longer an option. That door has long shut. The national debt would stomp down like an 800 lb gorilla, dragging the global financial system with it. If the American economy fails, there’s no superpower in the wings to save anyone. The only exit now is up.

That in mind, to not try something like DOGE seems riskier than to try and fail at it. Speaking for myself, I’ll take the folks who try every time, regardless of which party they work for. If a Democrat wins in 2028, they should try their own version of the same. Whether or not it was Einstein who first said it, we indeed cannot solve our problems with the same thinking we used to create them. When the status quo has failed, what's the civic virtue in staying the course? Especially when we can see where that course is headed.

Of course, others may reach different conclusions. I welcome them to show their work too. No debate was ever spoiled by too much sunlight.

Technically it’s not going to be an official department, but a temporary commission.

One major exception is “intermediate goods”. The sales of pepperonis and cheese to a pizzeria don’t count, while the final sale of every pizza does. This is just to avoid double-counting. While there are different ways of handling this, the point is to capture the final price wherever possible, as it’s the best reflection of the total value created along the way.

Every worker added into a job that doesn’t become more productive over time will eventually drag down real GDP per capita, and will ultimately cost the government more in benefits and services than they contribute in GDP-turned-taxes. While adding these workers can be good and necessary in some sectors some of the time, the goal should always be to either (1) gradually shift them and/or their children into higher-productivity jobs, (2) have them take useful jobs left behind by people moving into more productive ones. But both these things get harder over time.

Two percent or so is the normal goal for western governments, as it makes it a bit cheaper for them to pay back their debt over time. Going too far below this benchmark also tends to mean that the economy isn’t growing enough, which is a worse problem.

One counterpoint would be that a smart country might push their debt-to-GDP ratio aggressively to fund high-upside bets (like developing AI) that offer unusually huge payoffs in terms of future productivity growth. And there’s a possible future in which this is exactly what America did over the last few decades, where everything basically worked out. But there’s also a future in which AI and other breakthrough technologies simply didn’t unlock new productivity fast enough. Basically it’s an enormous gamble.

Lifespans may also increase even further if the current data on GLP-1s (eg. Ozempic) holds up. But even if people get healthier thanks to these drugs, this may not actually reduce their total healthcare costs, as it also means more total years over which they’ll need all types of healthcare. It may also reduce early deaths, which—though lovely!—also means further costs thanks to those extra years of collecting benefits.

When a company gets more productive, this extra value generally gets split between (1) higher ownership profits, (2) more R&D investment, (3) higher wages, (4) cheaper prices. The specifics depend a lot on how competitive the industry is.

Mind you minimum wages are more often increased at the state level today, not the federal. But the same dynamic applies there, and state deficits on a long enough timeline become a federal problem anyway.

The US owes itself about $7T of its $36T total federal debt. How? When you pay a dollar in eg. social security taxes, this dollar doesn’t go into a special social security wallet. The government immediately spends that dollar and then puts an IOU into said wallet instead. And that pile of IOUs has grown very large!

One of my clients, despite being a reasonably wealthy entrepreneur, quite literally did not know what Google was. This was in 2014 or so. Ask your local consultant for a zillion similar examples. The issue though is that these businesses quickly reach a growth plateau, and then that’s it.

One big one will of course be Congress. While the President can request cuts to any spending that Congress has already approved and appropriated, it’s then up to Congress to agree to this. The same rough logic applies to lots of other reforms Trump/DOGE may wish to push through. While the Republicans will have a majority in both chambers, they still need consensus—and will in some cases will likely need to break filibusters in the Senate.

Very interesting, thanks!